Tesla’s legendary CEO, Elon Musk, defiantly took his eyes off the road and stared into the sun after unveiling his “Master Plan” (“Part Deux”) on twitter last night.

In it, he officially announced his intention to “provide solar power” (facetiously adding, “No kidding, this has literally been on our website for 10 years.”)

But it still comes on the heels of a bid to merge Tesla and SolarCity, a solar energy and capture company.

In light of poor market performances from both companies, critics have said that, as far as Tesla is concerned, the move is not such a bright idea.

Cloudy days

According to Brad Erickson, a research analyst at Pacific Crest, the merger illuminates Tesla’s “downward sloping credibility curve” with its shareholder base.

Analysts have called the bid an “ill-timed” and “unneeded distraction”. Argus, a market research group, downgraded Tesla’s rating from BUY to HOLD because of the “meaningful risk” a company like SolarCity poses.

This isn’t hard to buy when you take a look at SolarCity’s 2016 first quarterly report. Its net loss outstripped its gross profit 21 times.

Its share price has been dropping accordingly, plummeting to $16.76 on its worst day this year.

Solarcity May 2016 by roserose on TradingView.com

Tesla in trouble

While SolarCity may be burning out, Tesla’s “not doing so hot” either.

At least that’s what Jonas Slaunwhite, a hedgefund manager at Citco Group Ltd. said when he took a look at Tesla’s 2015 Annual Report.

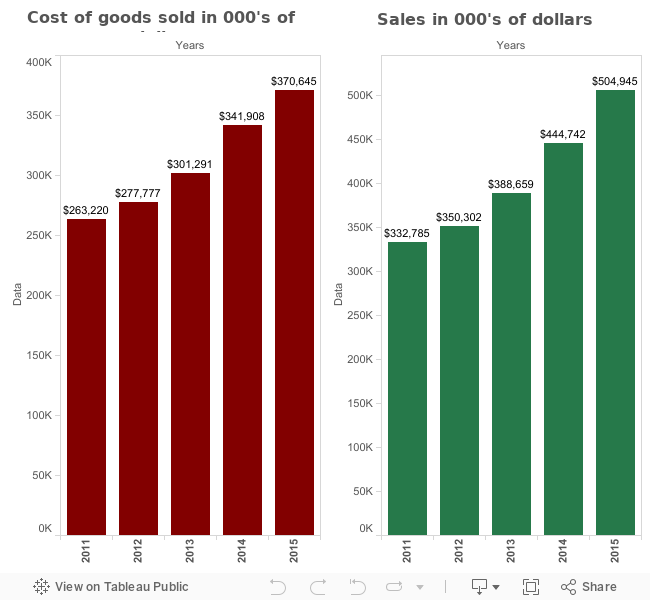

“Two billion dollars in loss…negative six dollars a share,” he mumbled to himself as he scrolled down. “That’s really just not good.”

Source: Tesla Annual Report 2011, 2012, 2013, 2014, 2015

SLAUNWHITE’S TOP FOUR CONTRIBUTING FACTORS:

1.“FEAR ON WALLSTREET”

The stock market has taken major hits on all fronts, from low oil prices to the financial exodus after Brexit.

“Low oil prices hurt a company like Tesla because they need electric to look like a cheaper alternative for drivers,” explained Slaunwhite.

2. A BIG PRICE TAG

Musk’s ultimate goal is to to create an affordable, high volume car. But with even the cheapest model starting at around $100 grand, his product simply isn’t within reach for the average buyer.

3. HIGH PRODUCTION COSTS

The Model 3, S and X’s high price tags come as a result of an extremely expensive production process. Despite having had a healthy gross profit in 2015, Tesla’s enormous operating costs slashed its bottom line.

Toyota had similarly steep expenses, but at least Tesla’s biggest competitor managed to make a profit. That year Tesla didn’t even break even.

Source: Toyota and Tesla’s 2015 Annual Report.

Slaunwhite blamed this on its hefty research and development fund, which ate away 17 per cent of its 2015 net revenue. But he also conceded that research is a necessary investment.

“If they can figure out how to improve their automotive’s…and make their cars for less,” he said, “they’re gonna sell more.”

4. SUPPLY AND DEMAND

While selling more cars is the goal, delays in supplies and deliveries contributed to Tesla’s consistent failure to meet production and delivery demand so far in 2016.

“GIGA” – the factory of scale

Reducing production costs and increasing efficiency will be essential if Tesla is to increase its output ten-fold by 2018 to 500,000 vehicles a year.

That’s exactly what Tesla intends to do at Gigafactory – Musk’s $5-billion, 13-million sq/ft. battery megafactory in the Nevada desert, according to the UK’s Daily Mail. It’s set to open July 29 – one week from today. Source: Electrek.co on Youtube

Gigafactory will ensure that lithium ion – the main ingredient in its batteries – costs less and lasts longer as an energy storage solution.

By bringing affordable, sustainable transportation to the mass market, Musk will be able to “achieve a sustainable energy economy” sooner than anyone ever imagined possible.

A “GOOD” FUTURE

While Musk conjures the vision of a greener future, some investors still only see the colour of money.

If the future really is all about “fiscal solvency”, then perhaps Erickson is right about Tesla. But Dr. Peter Harrop, Chairman at IDTechEx and co-author of “Electric vehicles, Forecasts, Trends and Opportunities 2016-2026”, is the one who is not convinced.

“Tesla is a leader in the design and commercialisation of pure electric cars,” said Dr. Harrop through email correspondence. “It lacks profit but has an orderbook that its competition can only dream about.”

Critics may call Tesla’s bid to acquire SolarCity “ill-timed”, but the only word Harrop had for the move was “strategic.” For Musk, it’s just one more piece in a bigger puzzle.

“The point of all this [is] accelerating the advent of sustainable energy, so that we can imagine far into the future and life is still good,” said Musk. “That’s what ‘sustainable’ means. It’s not some silly, hippy thing – it matters for everyone.”