It’s costing Canada’s leading dollar-store retailer more money to do business, according to figures released in its most recent quarterly report. And experts say that could cost consumers more money to shop there.

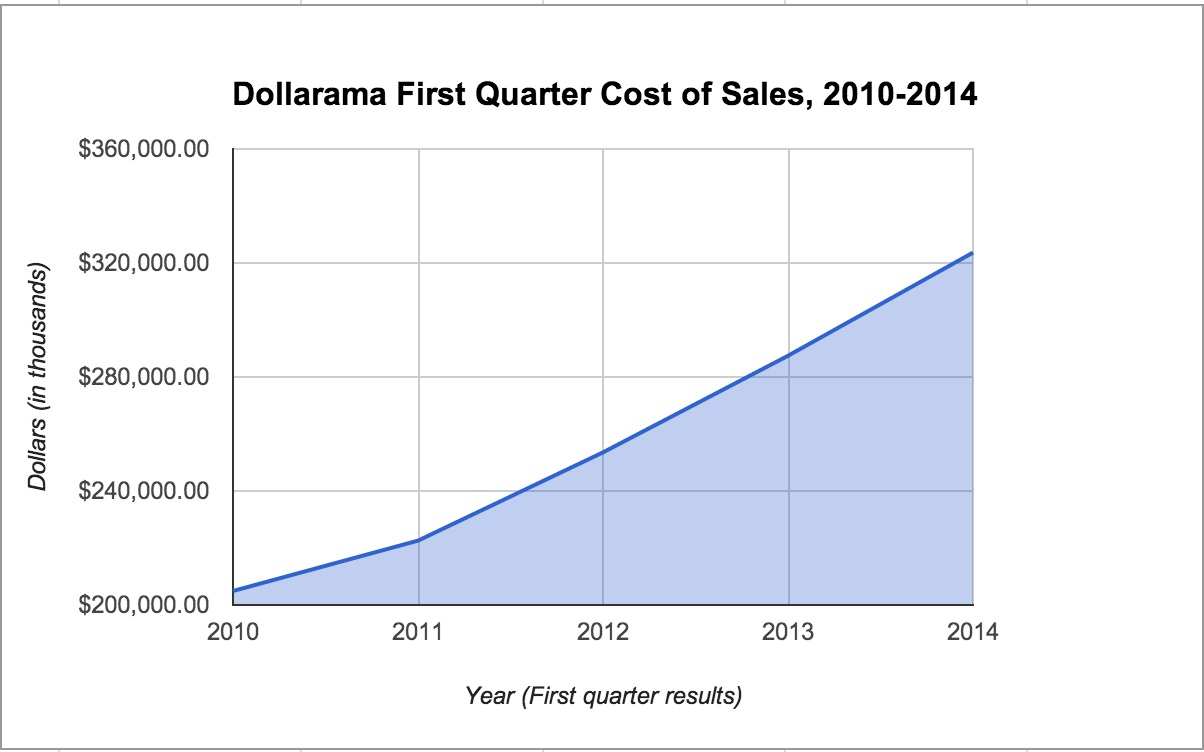

The cost of sales is a key indicator of a company’s health. It includes all costs directly involved in producing the company’s products. First quarter results for the past five years show that Dollarama’s costs of sales have steadily climbed, at an average rate of 12% per year.

Rather than looking at costs of sales as an absolute number, analysts measure them against actual sales. To do this, they calculate gross margin: the percentage of sales revenue that the company keeps after subtracting its costs of sales. Dollarama likes to keep its gross margin between 36 and 37 per cent, “as they believe this is the range that properly balances returns for shareholders (who want higher margins) and offering a compelling value to the customer (who wants lower prices, and thus lower margins),” James Allison, Scotia Capital retailing associate who follows Dollarama, said in an e-mail.

But this quarter, Dollarama’s gross margin fell slightly below that sweet spot, at 35.4 per cent:

Another way we can see those rising costs is by comparing Dollarama’s year on year growth of sales to cost of sales. The two have been growing at roughly equal rates – until this year, when their costs increased at a slightly faster rate than their sales. In the first quarter of 2014, sales increased by 11.8 per cent compared to a year earlier. But the cost of sales increased by 12.6 per cent, meaning growth in costs is slightly outpacing revenue.

In its most recent Management’s Discussion and Analysis report, Dollarama attributed these climbs in costs to some key factors: a weakening loonie and stronger Chinese renminbi, rising fuel prices that increase their shipping and transportation costs, and the upward climb of the Canadian rental market, which increases lease rates for their stores.

Two years ago, Dollarama started introducing items at $2.50 and $3.00, which it says helps them respond to fluctuating costs of doing business. But its latest annual report, released in April, warns that the company can’t predict whether the $3 price cap will be sustainable in the future. Dollarama “relies heavily on imported goods”, the report says, so economic fluctuations and political instability in their source countries could rapidly cut into its profit margins, especially when it’s working within such a limited price range.

https://www.documentcloud.org/documents/1275201-dollarama-annual-report-2014.html

Kai-Yu Wang, a consumer markets expert at Brock University’s Goodman School of Business, says similar economic factors are leaving dollar stores throughout North America at a crossroads: either keep prices the same by sourcing cheaper goods, or sell higher quality products with higher prices.

Wang believes Dollarama will choose the latter route. He says the company has already been experimenting with introducing a wider array of higher-priced items, and seeing how customers respond. “I think for them it’s trial and error right now,” he says.

If Dollarama decided to break its three dollar cap to stock pricier products, it would move into more direct competition with retailers like Wal-Mart and Target, says Wang. But he expects Dollarama will move slowly and watch “whether their existing target market can accept going to Dollarama if it’s no longer Dollarama”.

But other experts say there’s nothing to worry about in the company’s numbers. “There’s nothing alarming about these costs to me,” says Eric Dolansky, who teaches marketing at Brock University’s Goodman School of Business, saying the fluctuations in costs are relatively small. “To me, their rising costs are simply that they’re selling more stuff, so they have to buy more stuff to sell. ”

Beyond that, Dollarama is still an extremely profitable company, says Brent Barr, a Canadian retailing expert and instructor at Ryerson’s Ted Rogers School of Management. Their net income jumped 17 per cent from the same quarter last year, “It’s good, solid growth,” he says.

Dollarama could not be reached for comment.